It’s not going to be a good day for the global financial markets.

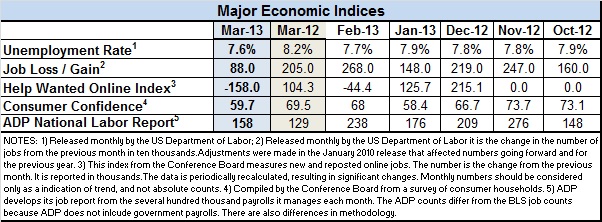

On Friday, the U.S. Department of Labor reported that March saw only 88,000 non-farm jobs added to the U.S. economy, the worst showing since last June and far below the 200,000 range economists were anticipating.

European financial markets dropped sharply after the Labor Department released the numbers, hitting a one-month low. In the U.S., the Dow Jones industrial average futures fell 143 points and S&P 500 futures were down nearly 17 points in the minutes after the 8:30 a.m. EDT report.

“A very weak labor market”

Investors were poised to act quickly, put on the alert Wednesday when ADP’s monthly estimate of private sector job growth came in at 158,000, which was also significantly below what economists expected. “This is a very weak labor market,” economist Martin Feldstein told CNBC after the report was issued.

Especially troubling was that the hiring slowdown came after months of growth that averaged almost 200,000. Last June, 87,000 jobs were added, but that was the only time since August 2011 that job growth dipped below 100,000.

SHRM’s Line Report, issued Thursday, predicts that next month will be much better. “In April, the service-sector hiring rate will reach a four-year high for the month, and more than one-third of manufacturers will add jobs,” predicts the monthly hiring survey by the Society for Human Resource Management.

CareerBuilder, which issued a second-quarter job forecast, was less aggressive, but still upbeat. Its survey of hiring manager and recruiters found 26 percent saying they expected to increase in their full-time, permanent headcount this quarter. However, the numbers expecting to hire more workers was less than in 2012.

Jobs report winners & losers

In the March jobs report, only a few sectors showed increases:

- Health care added 27,900.

- Temp services added 20,300.

- Leisure and hospitality was up by 17,000, with most of the growth coming in food service and hospitality.

- Professional and technical services added 24,600 jobs, with 10,700 in accounting and bookkeeping.

- Construction was up 18,000.

The biggest losers were:

- Retail dropped 24,100 jobs, with the biggest hits coming in clothing stores (-15,300) and building materials and garden supply (-10,100).

- Truck transportation shed 6,900 jobs.

- Financial activities as a whole dropped 2,000 jobs with some areas — commercial banking for example (-2,900) — down more. Minor hiring in the real estate and securities areas helped offset some of the job losses.

- Manufacturing lost 3,000 jobs.

- Government was down a total of 7,000. The federal government shed 14,000, mostly in the U.S. Postal Service. State education hiring offset some of the losses.

A half-million more dropped out of the workforce

The only good news in the March report was that the nation’s unemployment rate edged down to 7.6 percent from 7.7 percent in February, a four-year low, and adjustments to the previous job counts for January and February were upped by 61,000.

However, even that silver lining came on a dark cloud: nearly half a million workers dropped out of the U.S. labor force in March, accounting for much of the decline in the unemployment rate and causing the participation rate — the number of civilians working or actively looking for work — to fall to the lowest level since 1979.

Indeed, the actual numbers of the unemployed didn’t change during the month, according to the report. In March, 11.7 million were counted as officially unemployed, with 4.6 million out of work for more than half a year. The number of part-timers who wanted full-time work but couldn’t find it, declined by 350,000 during the month, leaving 7.6 million on part-time payrolls. Another 2.3 million workers want work, have stopped looking, and so aren’t included in the official count of the unemployed.

The picture to the north in Canada was equally bleak. The nation lost 54,000 jobs in March, its biggest one-month loss in more than four years. The unemployment rate rose to 7.2 percent, a four-month high.